Value Vs. Valuation: A Dilemma for Emerging Market Investors

Just one quarter ago, it felt like emerging markets might finally be turning the corner, with global growth inching higher and trade tensions between the U.S. and China showing signs of abating. But then came the swift global proliferation of COVID-19 infections, with the first case emerging in Wuhan, China, in December 2019. The pandemic radically altered the fortunes of many countries, companies, and individuals, with potentially lasting effects on many emerging markets.

Here in the U.S., the panic that capsized our markets back in March is starting to feel like a bad dream from long go. Emerging markets, however, have not been so fortunate. Despite the recent bounce, emerging market equities have declined nearly 20 percent since the start of 2020, compared with a 10 percent decline in the S&P 500. For a valuation-driven investor, this situation presents a compelling relative value opportunity. But the dichotomy between value and valuation must be clearly understood by emerging market investors.

Emerging Markets Defined

The MSCI Emerging Markets Index consists of equities in a diverse mix of 26 countries, and this diversity has never been so apparent. To understand the different levers that pull the various countries classified as emerging markets, we can divide the emerging market countries into four different complexes: the commodity suppliers, the goods manufacturers, the exotic vacation destinations, and the middle-class consumers. The economic effect of the global pandemic has likely been uneven across these complexes, owing to the varied path that the viral spread has taken, the varied measures adopted by the different countries, and the varied effect of an almost certain global recession on these countries.

The commodity suppliers. This complex consists of the classic emerging market countries that have historically been representative of the entire asset class. Several Latin American countries (e.g., Brazil, Mexico, and Chile) fall within this definition. Commodity exporters suffered the double whammy of a demand collapse and a supply shock. Global economic activity ground to a halt as countries entered lockdowns, reducing the demand for energy and other commodities. Further, Russia and Saudi Arabia embarked on a price war that led to the price of crude oil turning negative at one point.

For commodity-driven economies to recover, a strong cyclical global recovery is necessary. In the meantime, decisive governments need to take aggressive measures to contain the spread of the virus while also supporting their economies with fiscal and monetary stimulus. If the Brazilian response to the disease is any indication, we could have a health crisis brewing in the region, such that economic stimulus measures of any sort may become a moot point.

Goods manufacturers. This complex includes countries that are plugged into the global supply chain. Here, China has a big representation. But China’s dependence on manufacturing has reduced over the years, and a greater part of its GDP is now generated by domestic consumption. Countries that continue to generate substantial output from exports include the likes of South Korea, Taiwan, and Vietnam. These countries have done a commendable job containing the virus, thanks in large part to widespread testing and contact tracing. Thus, they have the potential to emerge from the crisis the fastest. Nonetheless, their fortunes depend on how quickly global demand recovers.

Vacation destinations. Next, we have emerging market countries like Thailand and the Philippines that depend heavily on revenues earned from travel and tourism. These countries have also been ahead of the curve in terms of disease containment. But with travel restrictions currently in place (and beyond), these countries will face a bleak outlook if tourists are not comfortable taking vacations to far-off destinations.

Middle-class consumers. Finally, we have what I think is the most exciting part of emerging markets: the complex and fast-growing consumers. Here, we have behemoths like China and India. China was first to enter the crisis and among the first to exit it. New daily cases in China have reduced to negligible numbers. Life is slowly returning to normal, although capacity use is still well below normal. India, on the other hand, is in the midst of the world’s largest lockdown, with daily case counts continuing to rise.

For middle-class consumers in these and other emerging countries, the pandemic could result in a massive blow to their discretionary spending. At a time of crisis, consumption is reduced to needs while wants are put off for later. Certainly, spending on technological tools to enable remote working and learning, online games to stay entertained, and so forth is likely to increase. But these middle-class consumers are not shopping in malls, eating out, or taking domestic and international vacations. Many are losing their jobs and cutting back on spending. A full return to normalcy in terms of consumption spending could take several quarters (if not years) and could set back upward mobility in several sections of the population.

Rising Macro Risks

Apart from China, most emerging markets do not have the health care infrastructure of the magnitude needed to contain a widespread pandemic. They also have limited monetary and fiscal capacity to put a floor on their capital markets. Increased indebtedness and dependence on foreign capital flows compound the pressure. Over the past decade, the official debt for the 30 largest emerging countries has risen 168 percent, to more than $70 trillion. Since the start of the coronavirus crisis, almost $100 billion of foreign capital has fled from emerging markets. Falling income, higher interest costs, and capital flight will make servicing and refinancing the debt difficult. With a significant proportion of the debt denominated in foreign currency, devaluation of emerging market currencies exacerbates the problem.

Finally, trade might reappear as a concern, with dissents rising about China’s role in the spread of the virus. The pandemic has made painfully explicit the downside risks of dependency on complex supply chains and might exacerbate the deglobalization trend already underway.

Mirage of Valuation Multiples

Given all of the above, investors will have to look hard to find value in emerging market equity investments commensurate to the risks undertaken. There are certainly diamonds in the rough that have been thrown out with the bathwater and are now available for sale. But it is harder to make a blanket statement for a compelling value opportunity for the entire asset class.

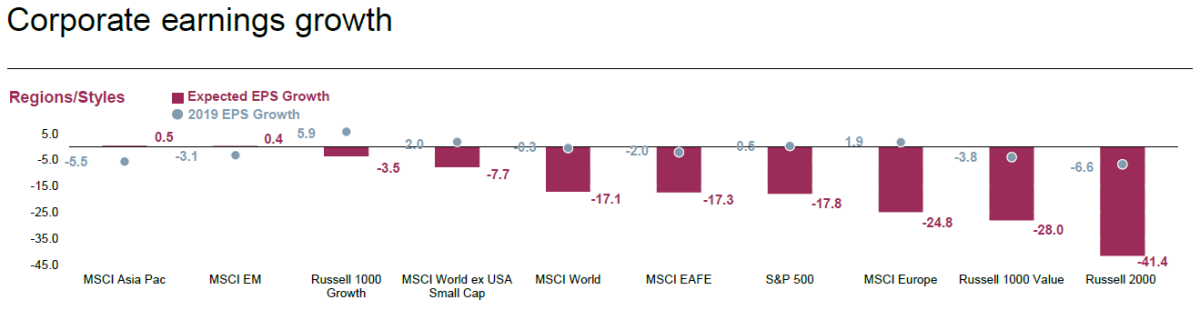

From a valuation standpoint, emerging market equities do appear to present an attractive buying opportunity. Still, we need to be very careful with that since forward earnings estimates for emerging market companies have not yet been fully reset to reflect the impact of the pandemic; hence, the valuation numbers might be giving stale signals. As illustrated in the chart below, consensus expectations for earnings per share (EPS) growth for the MSCI Emerging Makrets Index (as of April 30) were 0.4 percent, following -3.1% growth in 2019 and in stark comparison to double-digit declines expected in other major large-cap indices.

Source: FactSet

Beware of Landmines

One thing we do know is that this crisis will eventually pass, either by way of eradication or herd immunity. For markets that survive this period, we could see a credible and possibly a strong recovery. Within emerging markets, those with good health care systems, low debt, and low exposure to commodities and tourism could benefit from a pickup in global growth when the pandemic ebbs. In the medium to long term, emerging markets are likely to again grow faster than their developed market counterparts, as they will have that much more catching up to do. But emerging market investors must tread with caution and pick their spots carefully to avoid stepping on landmines and risking permanent loss of capital.

Editor’s Note: This original version of this article appeared on the Independent Market Observer.

The information on this website is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets.

The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. All indices are unmanaged and investors cannot invest directly into an index.

The MSCI EAFE (Europe, Australasia, Far East) Index is a free float‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of 21 developed market country indices.

Third-party links are provided to you as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites. Information on such sites, including third-party links contained within, should not be construed as an endorsement or adoption by Commonwealth of any kind. You should consult with a financial advisor regarding your specific situation.

Please review our Terms of Use.