2025 Midyear Outlook: For Fixed Income, Slow and Steady Wins the Race

Bonds had a solid start to 2025, with most high-quality fixed income sectors up low- to mid-single digits through the first half of the year. While stocks experienced a roller-coaster ride powered by policy uncertainty, fixed income generally held up well despite the broader market turbulence. Will it be the same story in the second half? Let’s take a closer look.

A Flock to Safety

Historically, investment-grade bonds have benefited in times of uncertainty, as investors often flock to the safety of high-quality fixed income when risks rise. We certainly saw that play out earlier this year when stocks sold off and bonds rallied. The chart below highlights year-to-date and one-year returns for a handful of major sectors within fixed income.

Year-to-Date and 1-Year Total Returns

| Year-to-Date | 1 Year | |

| Bloomberg U.S. Aggregate Bond Index | 2.35% | 4.61% |

| Bloomberg U.S. Corporate Bond Index | 2.40% | 5.13% |

| Bloomberg U.S. Corporate High Yield Index | 3.10% | 9.26% |

| Bloomberg Municipal Bond Index | -1.02% | 0.91% |

| Bloomberg Municipal High Yield Bond Index | 2.47% | 5.54% |

| Bloomberg U.S. Treasury 1-5 Year Index | 3.44% | 6.45% |

Source: Bloomberg, as of 6/10/2025. All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

Looking forward to the second half of the year, the most likely outcome for fixed income investors is continued solid gains. Still, there are risks that should be acknowledged and monitored, including the threat to the bond rally posed by increasing concerns about the country’s deficit and long-term debt plans.

Shifting Focus to Long-Term Yields

When will the Fed start cutting rates? Coming into the year, that was one of the major questions for the bond market. We entered the year with traders pricing between one and two interest rate cuts in 2025, with the first cut expected in May due to an anticipated economic slowdown. But this rate cut never materialized. The economic data showed the job market remained impressively resilient through the start of the year, while inflation remained stubbornly high. Fed members, including Chair Jerome Powell, have indicated the central bank is in no rush to adjust interest rates and will remain data-dependent when setting rates at future meetings.

Given the lack of Fed activity to start the year and muted expectations for further rate cuts in 2025, investor focus has shifted toward the longer end of the yield curve. This shift became especially apparent after Moody’s downgrade of the U.S. economy in May amid the ongoing congressional budgeting discussions that are set to expand the size of the deficit and national debt.

Long-term Treasury yields fell throughout the first quarter of the year. In the second quarter, they rose notably, with the 30-year Treasury yield hitting a recent high of nearly 5.10 percent in late May. While long-term yields have pulled back modestly from recent highs, they still sit well above the levels seen throughout 2024, indicating continued investor concern. Upwards pressure on long-term yields could present a headwind for fixed income investors in the second half of the year, especially as congressional negotiations over the budget and tax policies continue.

A Look at Corporate and Municipal Bonds

While Treasury yields attracted most of the attention in the first half of the year, there are compelling opportunities in the corporate and municipal bond markets for investors willing to take on credit risk in exchange for heightened yields.

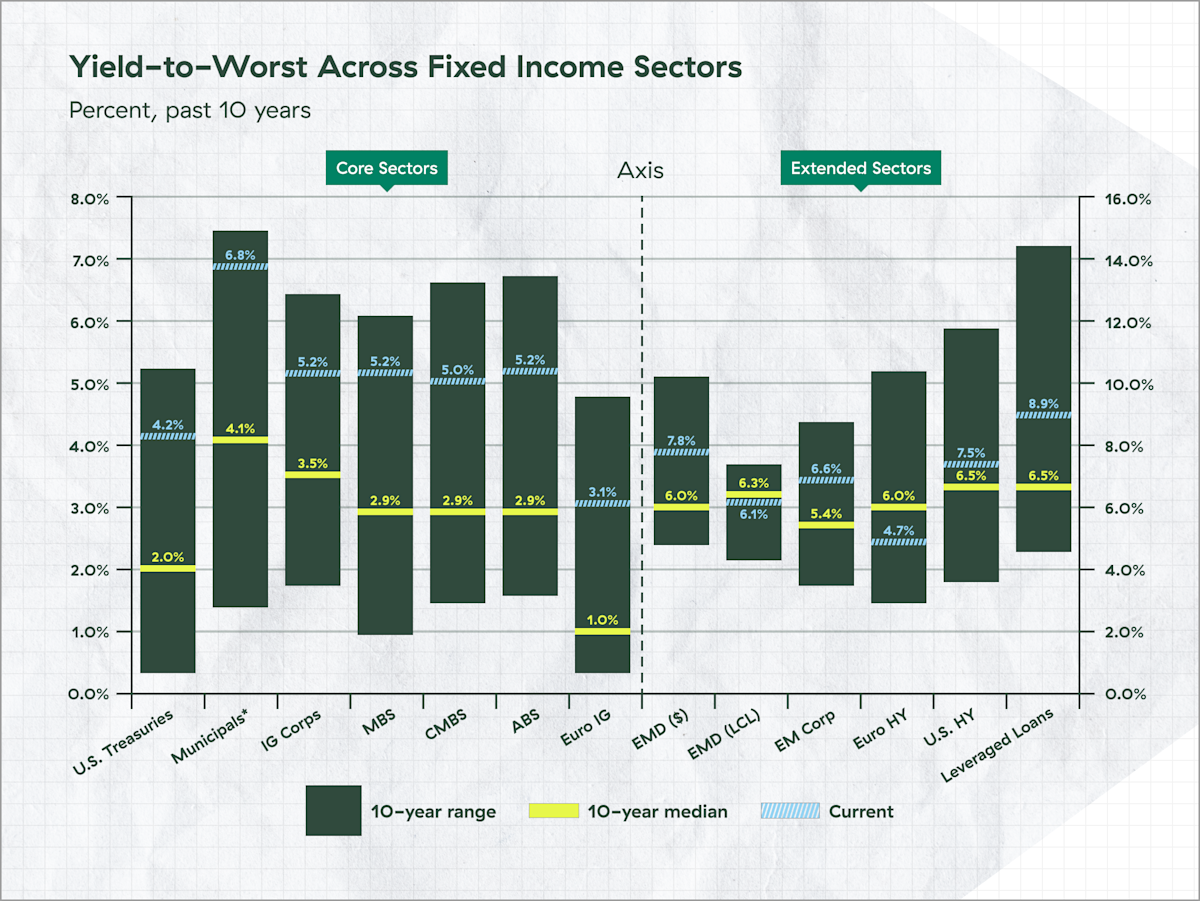

Treasury, municipal, and corporate bond yields are all currently above their respective 10-year median values (see chart below). But tax-adjusted municipal bonds and investment-grade corporate bonds may provide more potential yield compared to Treasuries.

Source: Bloomberg, FactSet, J.P. Morgan Credit Research, J.P. Morgan Asset Management. Indices used are Bloomberg except for ABS, emerging market debt and leveraged loans: ABS: J.P. Morgan ABS Index; CMBS: Bloomberg Investment Grade CMBS Index; EMD (USD): J.P. Morgan EMIGLOBAL Diversified Index; EMD (LCL): J.P. Morgan GBI-EM Global Diversified Index; EM Corp.: J.P. Morgan CEMBI Broad Diversified; Leveraged Loans: JPM Leveraged Loan Index; Euro IG: Bloomberg Euro Aggregate Corporate Index; Euro HY: Bloomberg Pan-European High Yield Index. Yield-to-worst is the lowest possible yield that can be received on a bond apart from the company defaulting and considers factors like call provisions, prepayments and other features that may affect the bonds’ cash flows. *All sectors shown are yield-to-worst except for Municipals, which is based on the tax-equivalent yield-to-worst assuming a top-income tax bracket rate of 37% plus a Medicare tax rate of 3.8%. Guide to the Markets – U.S. Data are as of May 30, 2025.

While investment-grade corporate bonds have moved in line with the broader market so far this year, investment-grade municipal bond returns lagged their peers in the first half. This underperformance was largely due to a combination of high issuance and choppy investment flows, along with concerns about potential tax policy changes that could strip some municipal issuers of their tax-exempt status. Looking forward, these headwinds are expected to turn into tailwinds for investors, as municipal bond valuations appear relatively attractive due to the recent underperformance.

Bonds Acting Like Bonds

Ultimately, the first half of the year was largely positive for fixed income investors. Despite the ups and downs for stocks, bonds held up relatively well in comparison. Given the policy volatility to start the year, it’s encouraging to see bonds acting like bonds in times of market uncertainty. We should expect to see that behavior continue in the second half.

That’s not to say there aren’t any risks to this outlook. Political uncertainty remains the most pressing issue for investors. While we’ve seen progress in lowering the temperature of the ongoing budget and trade negotiations, further surprises or disruptions could rattle markets. Fixed income investors may also face economic headwinds, especially if there is a sustained rise in inflationary pressure.

While high-quality bonds have historically performed well in times of uncertainty, recent history has shown periods where bonds and stocks experienced declines at the same time. Most recently, in 2022, a surge in inflation and interest rates led to double-digit losses for both stocks and bonds. While it’s not anticipated at this time, if we do see a meaningful rise in inflation, it could negatively impact markets, especially if it prevents the Fed from lowering rates later in the year.

Cautious Optimism Ahead

All that being said, fixed income investors should be cautiously optimistic as we enter the second half of the year. Valuations are solid, yields are compelling, and bonds are acting like bonds again. These factors should contribute to a solid rest of the year for investors.

Bonds are subject to availability and market conditions; some have call features that may affect income. Bond prices and yields are inversely related: when the price goes up, the yield goes down, and vice versa. Market risk is a consideration if sold or redeemed prior to maturity.

The information on this website is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets.

The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. All indices are unmanaged and investors cannot invest directly into an index.

The MSCI EAFE (Europe, Australasia, Far East) Index is a free float‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of 21 developed market country indices.

Third-party links are provided to you as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites. Information on such sites, including third-party links contained within, should not be construed as an endorsement or adoption by Commonwealth of any kind. You should consult with a financial advisor regarding your specific situation.

Please review our Terms of Use.